Foreword

In 2019, crypto was a small and insignificant market in the middle of a long winter. We had just started Sigil Core with three co-founders and a humble AUM. Bitcoin's market cap was below $100bn, prices were depressed, and everyone expected the whole thing to die.

I remember the urgency and excitement of that moment. Crypto was the best asymmetric bet I'd ever seen — risk 1 to win 50, a true generational opportunity. But pitching that thesis was surreal. The post-ICO bear market had written crypto off, and almost nobody saw the upside. I felt like either I was crazy, or everyone else was.

Raising money was all but impossible, especially without any track record or relevant pedigree - unless you want to count my poker pro career. What we lacked in those areas, we made up for with grit, vision, and curiosity. We dug deep into the world of crypto, blockchains, and DeFi, and soon became one of the leading funds in the industry.

Seven years later, the thesis has largely played out. Sigil Core's total upside is approaching my rough initial estimations. I still believe blockchain adoption winners will be one of the best-performing investments of the next decade. Much like FAANG kept outperforming everything else post-dotcom. But we honestly cannot call it a 1:50 anymore. We're entering the stage where scale and distribution matter more than tech breakthroughs, and winners will keep winning.

The AI trend in 2026 is not the crypto trade of 2019. I feel the same urgency to invest, but the idea is far from contrarian. Basically everyone agrees AI is meaningfully changing the world, for better or worse, and every investor wants exposure.

I was lucky enough to buy NVDA and PLTR reasonably early — in 2022 and 2023, when I saw the first signs of generative AI hitting escape velocity. My thesis at the time was rudimentary. I had a gut feeling this was going to be huge and I needed to participate. My understanding of AI, LLMs, infrastructure, and supply chain was limited, and it took me two years of catching up to shape a real thesis around the technology. But the original intuition about AI being the most impactful digital breakthrough since the internet is proving correct.

When I proposed Sigil Supernova to my partners, it was with the same urgency I felt in 2019. We spent a lot of time on this decision. We have a strong track record navigating a regulated fund through a wild crypto market. We've survived multiple cycles and brutal bear markets and come out on top. We're well positioned to capture the ongoing adoption trend. So why not stay in our lane?

The answer: we realised our DNA isn't just "crypto investors," it's disruptive tech investors. We invest in new technologies because they offer the biggest opportunities to grow and the least efficient markets to compete in. Crypto was one such industry for the past 10 years. More are emerging now, led by AI proliferation.

Even if we didn't launch Sigil Supernova, we would still invest our own money in this space on the side. So we might as well do it properly and build a new cell under Sigil Fund. Sigil is a "forever company" for us. We started it basically from zero, hustled like crazy to succeed, and managed to scale it up to one of the world's leading crypto fund brands. We have the majority of our net worth in Sigil, and most of our friends are invested in at least one of our vehicles. So naturally, we manage it with maximum skin in the game and passion.

But let's humbly come back down to earth. We start by acknowledging our limitations. Our track record in crypto is very decent, but that doesn't necessarily translate outside of it, in the world of deep tech and AI. It's Day 0 for us. Along the way we've learned many important lessons about public and private markets, about disruptive technologies and their hype cycles. Yet there is much more we are still learning.

How are we thinking about Supernova's place in the investment world? Why would we want to invest our money actively rather than just buying an index?

Active investing is in our blood. It provides a necessary feedback loop to the market. It gives us agency, forces us to challenge our assumptions, and pushes us to improve and grow as investors across the board. We are making conscious, opinionated bets on human ingenuity and technology as the main sources of progress. We are also making a conscious, opinionated bet on our own ability to actively identify the dominant trends and opportunities in the next decade.

On the public side, we aim to generate performance by forming a granular, path-dependent vision. Not only of AI proliferation, but of adjacent tech opportunities shaping the progress of humanity in the next 5–10 years.

The portfolio we're building is designed to:

- Profit from the identified trends and their bottlenecks.

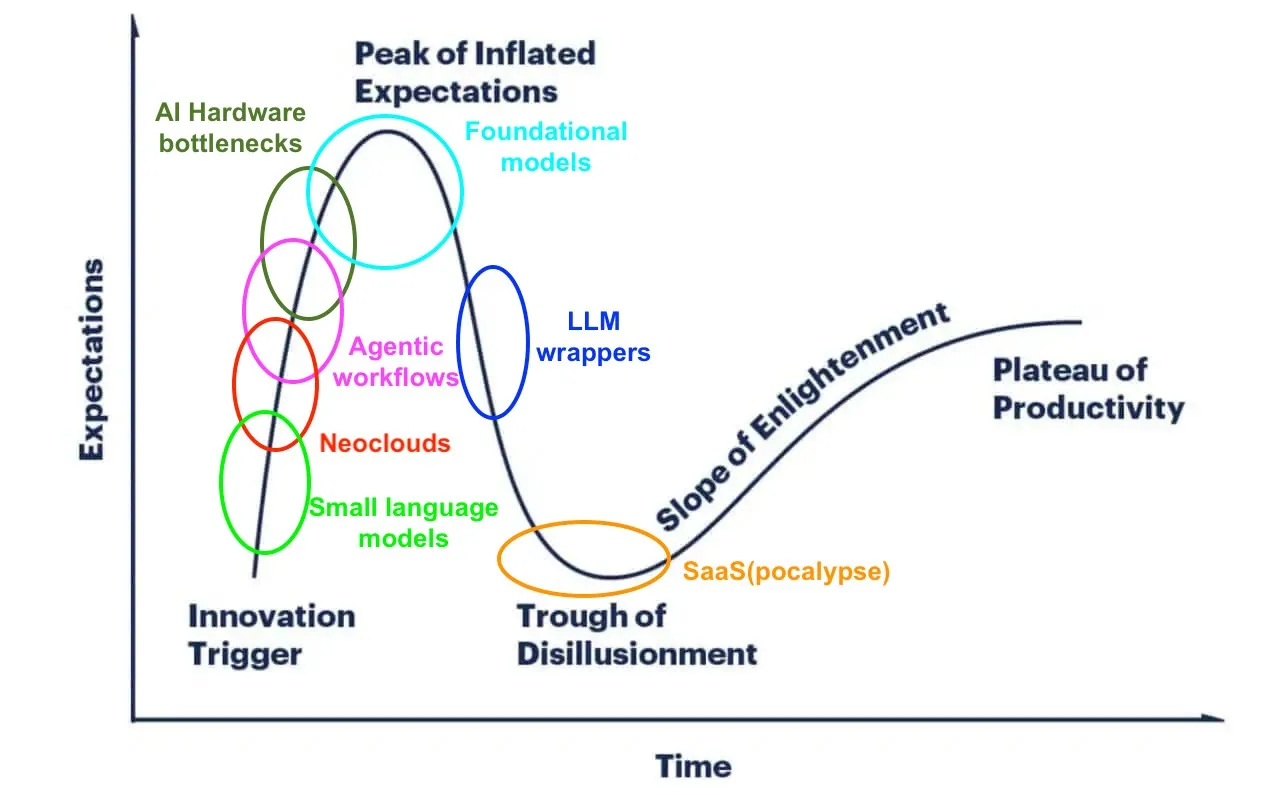

- Reflect the technology lifecycle — from hyped expectations, through the trough of disillusionment, toward the plateau of productivity.

- Cover the best opportunities across the stack, from seed-stage startups to public equities.

- Maintain liquidity across a large portion of the NAV — both for us and for outside investors.

- Stay deliberately more diversified, to avoid being "directionally correct with our general thesis but backing the wrong horse." (as we shape up our thesis, we may move to more concentrated portfolio over time)

The questions we're asking to get there:

- Where do the biggest changes and re-pricing events occur?

- Which segments are disrupted and which face tailwinds?

- What are the second and third order effects of AI proliferation?

- How do we differentiate hype pumps and bubbles from secular re-pricing?

- What are the key bottlenecks, and who benefits from them?

One last question worth addressing: if we're managing our own capital, why raise outside money at all? Frankly, we don't need to. But a bit more size helps us into more competitive private deals, and we have a network of investors who want exposure. So we're opening it up, selectively.

Sigil Supernova Thesis

The LLM breakthrough is the most consequential technology shift in a generation. Knowledge work, procedural intelligence, and digital content (including code/software) are becoming commoditised.

When intelligence itself is commoditised, the bottleneck moves to the physical layer. In the past 20 years asset-light digital businesses ruled. The next decade will favour hard capital assets. That's why Nvidia is now the most valuable company in the world and the rest of Mag7 is playing catch-up, pivoting from high-margin digital cash cows into the largest CAPEX spenders on the planet, racing to secure scarce physical inputs.

The future winners are capital owners: those controlling AI computation, proprietary datasets, hard assets, and distribution. And alongside them, the operators who use cheap intelligence to widen the moats they already have.

If AI lives up to the hype, the second-order effect is just as interesting: heavy R&D moonshots become investable in a way they haven't been before. Biotech, new forms of energy, space exploration… Anything bottlenecked by the cost and pace of human cognition gets a structural tailwind. Deeptech "sci-fi" investments, while still “hard”, become more viable than ever before.

A counter-intuitive call: we think AI unlocks won't favour new software startups as much as established tech companies: incumbents with proprietary data, domain expertise, distribution, brand, or regulatory lock-in have everything they need to run agentic workflows on top of moats they already own. Pure software startups will struggle to displace them in most categories.

Cybersecurity and AI/agentic infrastructure are among likely exceptions, because they work with the biggest points of change that AI brings to the table. In general we think the most interesting startups of the next decade will be in hardware.

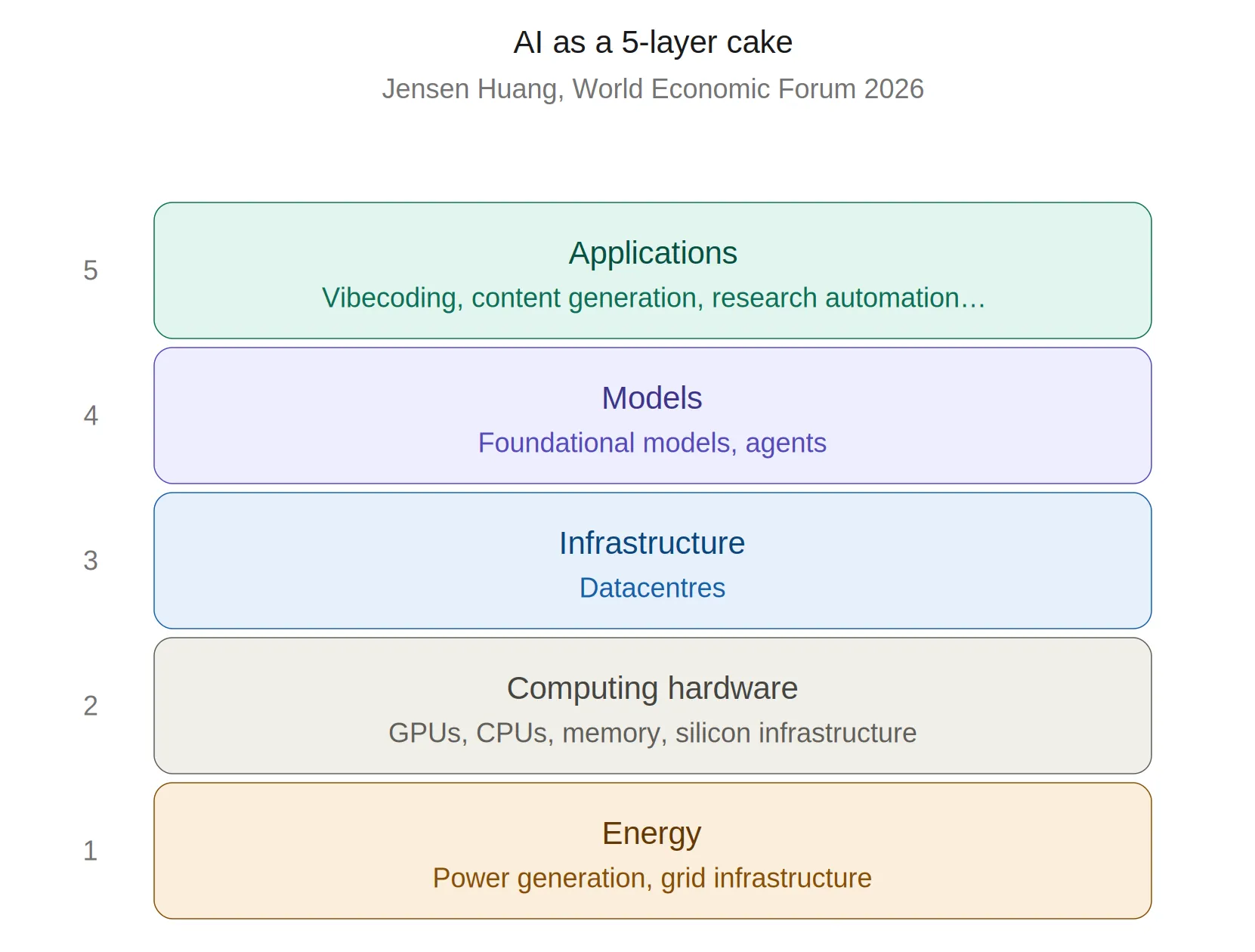

That's the lens we view the overall landscape through. Our portfolio will be structured as a flexible mix of public and private investments, anchored in 7 themes:

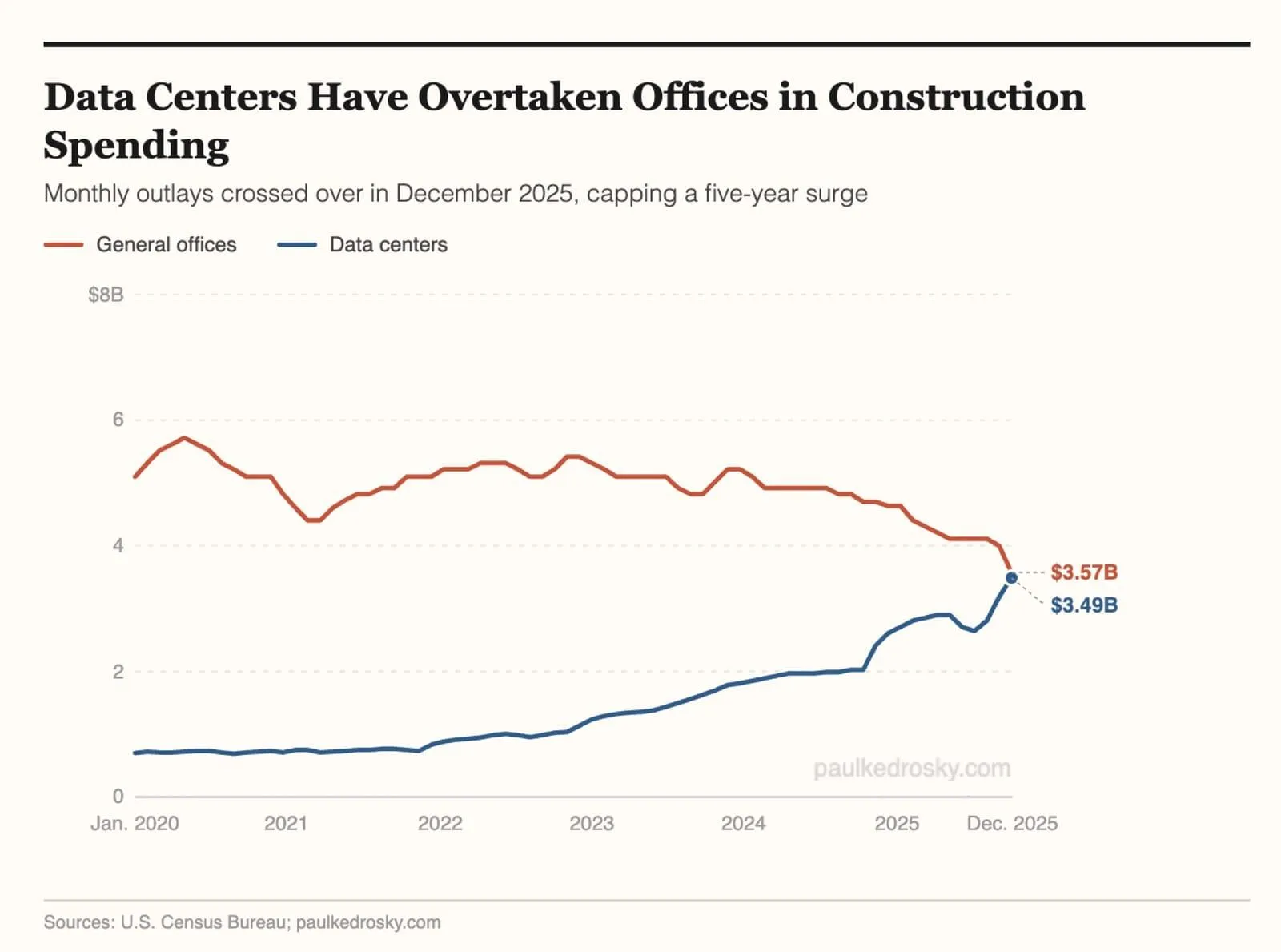

1. Datacentres — Building the artificial gigabrain

Trend: AI datacentre buildout is the defining capex story of this decade. A multi-year secular trend driven by two compounding forces. Hyperscalers are spending hundreds of billions to stay competitive and secure the vital AI computation resource. On top of that, sovereign nations are also investing heavily to not fall behind in the technological race. Compute has become both commercially vital and strategically crucial infrastructure.

The first to re-price were GPU companies, led by Nvidia. Memory manufacturers (NAND, DRAM, and HBM) are next - you may have seen the term "memory wall." CPUs are right behind them, as some of the computation moves to edge devices and agentic workflows turn out to be CPU-hungry. Photonics is also entering a productive phase, providing a viable alternative to copper-based interconnect in datacentres — with early signs of photonic chips becoming viable.

This hardware trend has been in full swing since 2024, and industry data points to a systemic demand overhang until at least mid-2027.

Bottlenecks: GPU, CPU, memory and adjacent components; the broader semiconductor supply chain, manufacturing, and energy; key materials and their processing; geopolitical risks.

Our take: The "silicon brain" is physical. AI can generate infinite digital outputs, but it can't create atoms from thin air. It needs energy. It needs processing power. It needs memory and the wiring (copper and optical) to move data around. It needs packaging and cooling. And it needs large, specialized datacentres built AI-native from the ground up — repurposing existing cloud infrastructure isn't enough. Specialised AI first datacentres called Neoclouds are emerging. Interestingly, Bitcoin miners specifically are sitting on viable datacenter facilities and cheap energy contracts. Because of the energy and hardware intensive nature of Bitcoin mining they are able to re-purpose their infrastructure for AI compute and become Neoclouds.

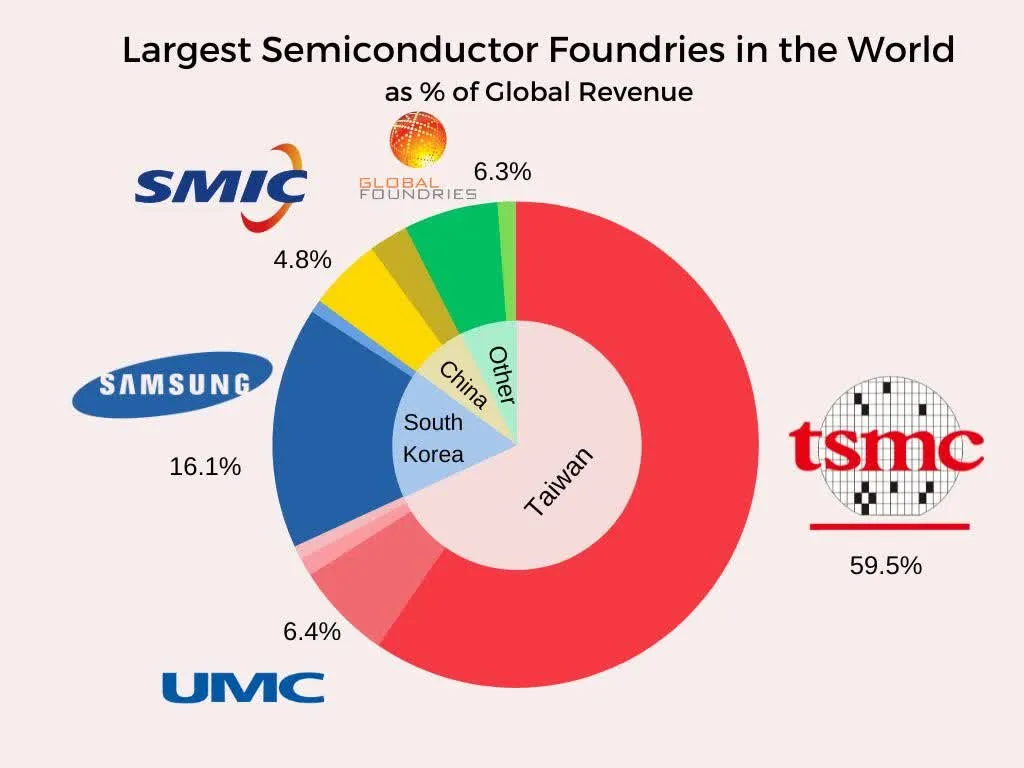

Basically each of the inputs mentioned above is a bottleneck and a beneficiary. The first-order winners are the manufacturers at the top of the stack: ASML, TSMC, Intel, Nvidia, Samsung and companies downstream from them. In several categories, their capacity is already booked into 2028.

Second-order: Neoclouds and datacentre infrastructure providers: Cooling (water cooling for GPUs is the choke point), energy enablers (mostly behind-the-meter generation), and the infrastructure to deliver power (grid, fuel, transformers).

Third-order: the materials underneath all of it. Copper for wiring and grid expansion, rare earths for magnets and motors, and the metals tied to grid-scale storage. Two to three decades of Western under-investment in the "dirty businesses" of commodity mining and midstream processing resulted in them becoming another physical bottleneck.

Alongside the centralised buildout, we're tracking the opposite trend: edge inference, AI computation running locally on-device. Niche today, but a meaningful one over the next few years, especially as specialised SLMs (Small Language Models) get cheaper and more capable. The logic is straightforward: a self-driving car doesn't need to be a generalist that writes complex code and does financial research. It needs fast reaction time, a low-latency sensory model, and an up-to-date map of the area. Your car's digital brain will specialise in getting you safely from A to B without needing to beat Magnus Carlsen in chess on the way there.

Layered on top of all of this is geopolitical risk that could turn into a really big bottleneck: Hormuz, rare earths, and Taiwan's role as the single point of failure in the global semiconductor supply chain. We'll return to these in the warfare theme and the bear case.

2. Application layer — Using the AI gigabrain

Trend: AI companies are aggressively growing and fighting for market share. Thanks to this, we live in a golden age of subsidized computation. But this won't last forever. Computation will become a major expense and software engineers, designers, and knowledge workers in general will need an "AI token budget". Low-value tasks will be priced out or pushed towards cheaper, open-source models.

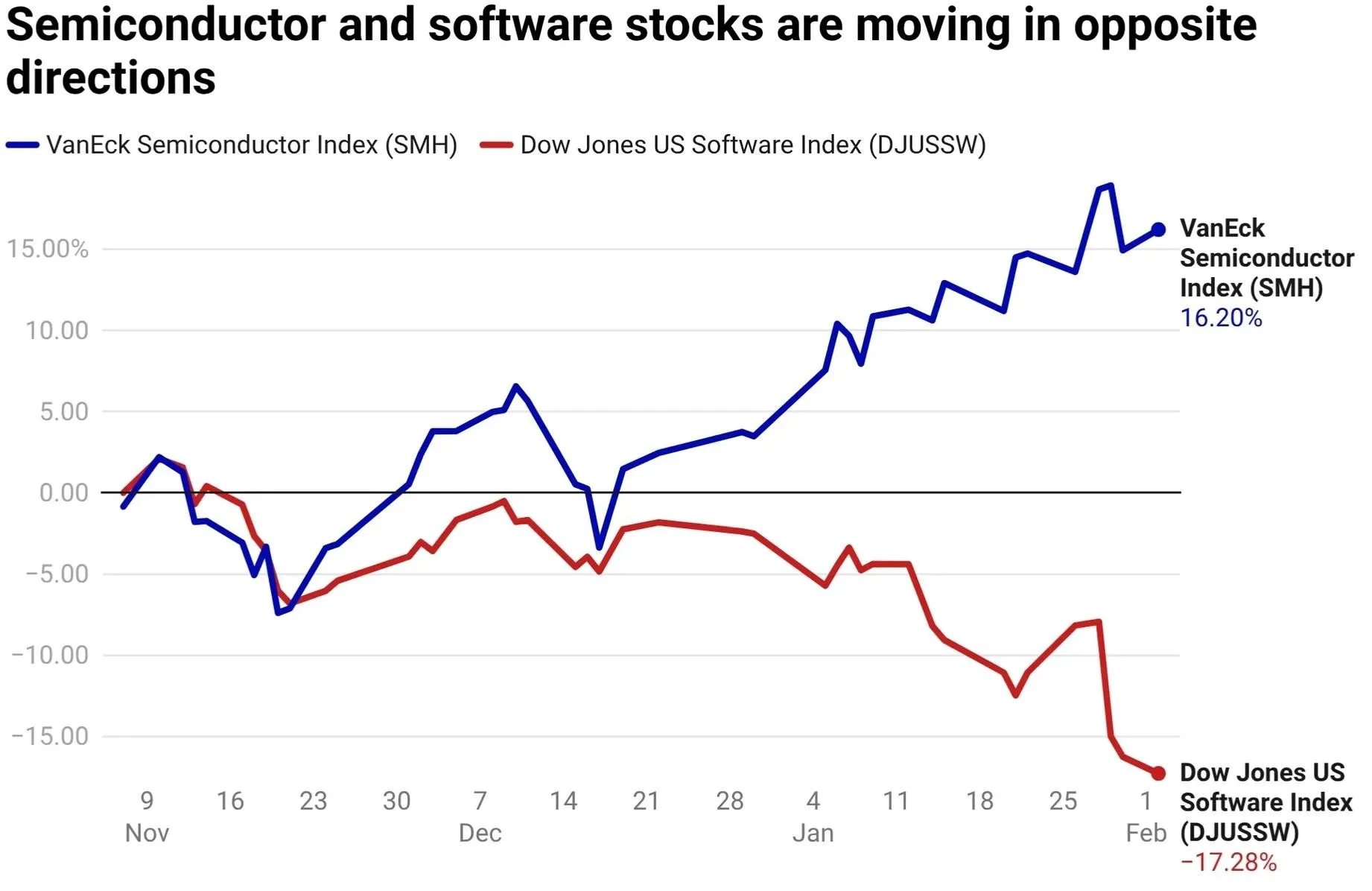

As AI computation becomes a more meaningful part of OPEX, human knowledge work commoditizes in parallel. Leading companies to hire less and restructure their workforce. Asset-light software companies that dominated the markets since the dotcom era are being repriced, and many will be forced to change their business models.

On the other side, individuals and small capable teams will coordinate faster and accomplish more with AI. We'll see humans using AI to boost productivity, alongside AI agents navigating digital environments and working independently. Agentic workflows will spread across industries. Businesses with AI-resistant moats will become more efficient and expand their margins. Human-light is the new asset-light.

Bottlenecks: the technical layer (compute, data, model quality and hallucinations), the externality layer (AI-related cybersecurity threats, regulatory hurdles), and the political layer (censorship, gatekeeping, social backlash).

Our take: The first-order trade, buying the labs and their LLMs, is consensus and priced for perfection. The more interesting bet is one layer down. Neoclouds and computation infrastructure providers are absorbing the demand the labs and hyperscalers can't serve themselves, and most are sold out: GPU capacity is booked through 2026 and well into 2027. This is the same demand we identified in the datacentre theme, but expressed at the operator level where the computation scarcity gets monetised.

When most people hear "application," they picture end-user software — a mobile app, a website, something with a screen. Agents are challenging that paradigm. An AI application may not look like an app at all. It may look like a swarm of agents: autonomous entities moving through the digital space, working independently, talking to APIs and databases directly without ever needing a UI.

But agents need infrastructure of their own. They need bandwidth and reliable ways to interface with digital systems. They need an orchestration and governance layer to keep them coordinated and in check. They need human-in-the-loop oversight. And they need a way to transact autonomously — that matters more than people realise. Agentic payments (autonomous AI entities sending and receiving value on behalf of users and other agents) is one of the application-layer opportunities where our crypto-native expertise translates directly.

The market is currently pricing SaaS for extinction. Our view is more nuanced: the disruption is real, but unevenly distributed. The companies most exposed are those whose primary moat is the user interface, workflow software, design tools, anything where the friction of "doing it yourself" was the reason customers paid. Agents collapse that friction.

The companies on the right side of the trade are those whose moats sit in proprietary data, distribution, regulatory lock-in, or workflow integration depth. For them, AI is a tailwind: lower headcount per dollar of revenue, faster product iteration, expanding margins, and the ability to roll out agentic features on top of existing customer relationships. The same dynamic that disrupts the UI-moat cohort entrenches the data-and-distribution cohort further. We're focused on identifying the second group at distressed valuations created by the first group's selloff.

3. Robotics and automation - Giving the AI a body

Trend: Despite the dominance of the digital economy and software in tech investing in the last 20 years, 70% of the world's economy is still physical. With the western demographic no longer growing as fast as in the last century, we need to replace as much human physical labour as possible with intelligent machines. Thanks to increased capabilities in AI, we can now achieve a higher level of automation than before.

Robotisation is the next meta for many industries including transportation, manufacturing, farming, defence, security and services. After two decades of unfulfilled hype, even self-driving vehicles are finally entering a productive stage, at least in some tech friendly cities such as Shenzhen and San Francisco.

Bottlenecks: key components, precision manufacturing, magnets and cameras, world models and navigation software, regulatory framework.

Our take: While the investing world is focused on the most hyped and crowded vertical, Humanoid robots, we are looking to invest in more practical use cases. All the robots, no matter their form factor, require components such as HD cameras, magnetic joints, local inference units, coordination and orchestration software, servicing…

The industries robots are disrupting first are surprisingly some of the more overlooked ones. Lower margin industries where cost (and safety) of labour is a bottleneck, such as agriculture, heavy manufacturing, mining and midstream processing. Before we will see humanoid robots populating our street and serving us tea in our homes, we will have specialised robots forming the invisible backbone of our key "hard" industries.

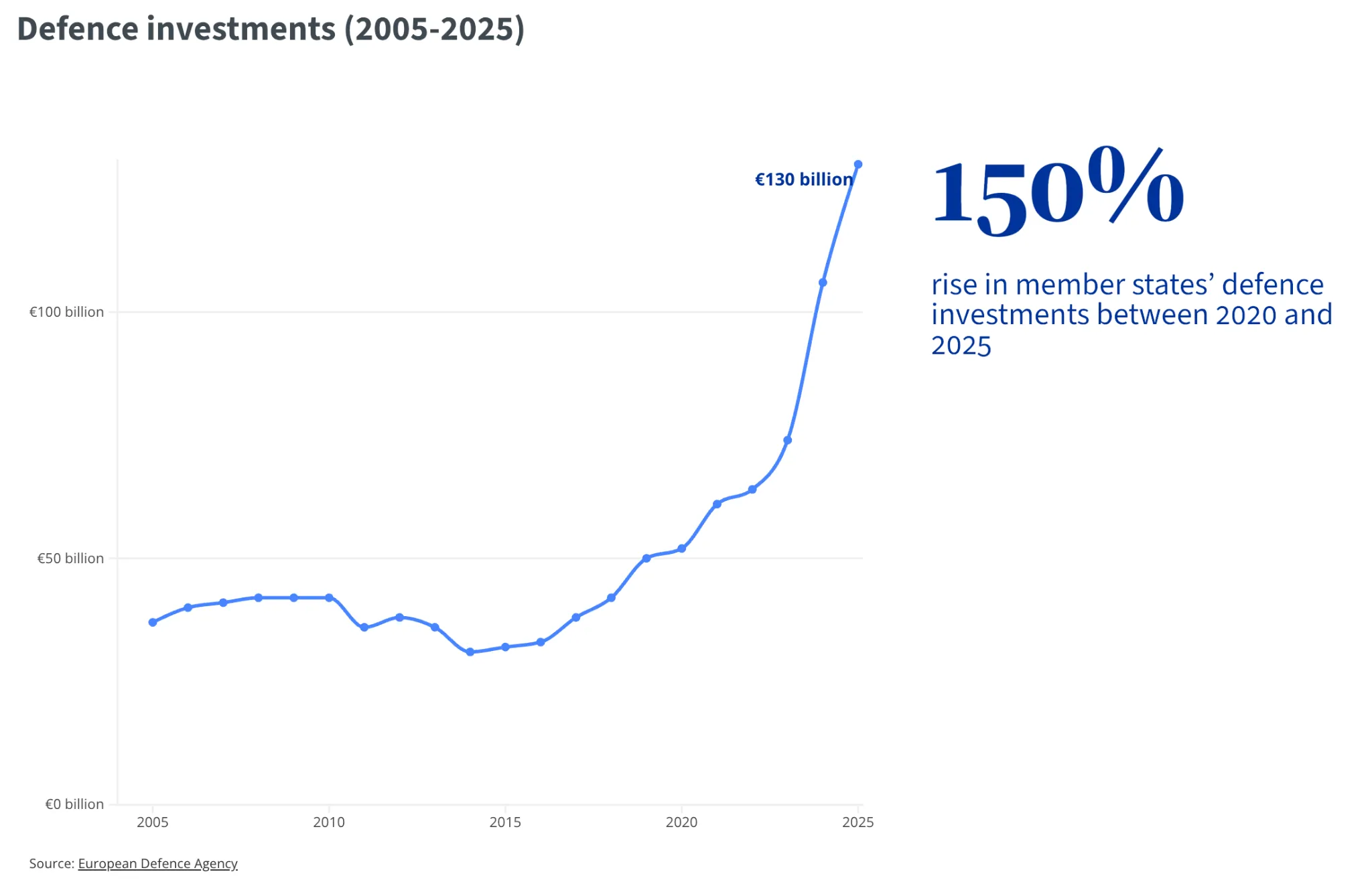

4. Future of warfare

Trend: For Western civilization to thrive, it needs to remain competitive on the field of battle. NATO defence budgets are rising to levels unprecedented since the Cold War. European defence specifically is waking up, prodded by Russian aggression in Ukraine and US shifting (some would say faltering) its commitments towards NATO.

At the same time, militaries everywhere are absorbing the lessons of the Ukraine war and the Hormuz crisis: automated systems and low-cost attrition are the future of warfare. The economic asymmetry is brutal. A modern Ford-class aircraft carrier takes 12 years and $13bn+ to build, and 4,500 crew to operate. It can be destroyed in hours by a handful of autonomous aerial and naval drones — costing a few million dollars, built in weeks, with zero lives at risk on the attacking side.

The other end of the curve is the opposite story. High-precision weapon systems are getting better at striking high-value targets while reducing civilian casualties. That’s a different kind of asymmetry, where capital and software replace volume.

Down the defence supply chain, we are observing Chinese efforts to chokehold critical materials - commodities such as tungsten and rare earths, and their processing. As mentioned in the datacentre theme, Western countries and investors overlooked these "dirty" industries for decades. It has become clear that reshoring and supporting them is a strategic necessity, especially for the defence sector.

Bottlenecks: key materials and commodities; bureaucratised procurement and the big defence contractor innovator's dilemma; geopolitically and strategically motivated trade wars and embargoes.

Our take: We're investing across the dual-use and defence value chain — focusing on the new technologies and approaches. On the offensive side: autonomous drones, missiles, and energy weapons. On the defensive side: early drone detection and cost-efficient anti-drone systems. In between: high-precision, low-collateral-damage weapon systems; orchestration and simulation software; battlefield energy delivery; ISR; and decision-support tooling for the operators using all of it.

Battlefield connectivity, real-time data and intelligence, AI powered decision making are where modern conflicts are increasingly decided — and where the innovator's-dilemma gap between primes and startups is widest.

We're also positioned for the structural overlap with theme 5. Space technologies are no longer just about intelligence and communication; orbital defence is becoming a real category and consideration for national security.

To find the best early-stage projects building the future of European and Ukrainian defence specifically, we backed Darkstar.

A note on ethics. We will only back opportunities tied to NATO countries and countries ideologically aligned. We hope for a future without wars — but if there must be conflicts, we hope they're between machines and precision weapons, with no human casualties, civilian or military.

5. Space Race 2.0

Trend: Three forces are converging on the aerospace industry. First, costs have collapsed. Since 2020, humanity has launched more satellites into orbit than in the previous six decades combined. SpaceX's reusable rockets brought the cost of payload to orbit down by two orders of magnitude, and Starlink has demonstrated that satellite constellations are now both commercially viable and strategically critical. Ukraine made that case visible to the world.

Second, a new space race is forming. US-China tensions are pushing both powers to re-think space strategy. The US announced the intent to build Golden Dome, a missile defence system partially based in space, with cost estimates ranging from $185 billion to $3.6 trillion depending on scope. Weaponisation of orbit is surprisingly trivial: at orbital speeds of 7.8 km/s, a simple 1kg mass carries the destructive power of a high-velocity missile without needing a single drop of explosive. This reframes orbital infrastructure as a strategic priority for defence, not just communications and observation.

Third, AI is creating new demand. Compute and energy bottlenecks have driven serious proposals for orbital datacentres — in theory providing constant solar power, "natural" vacuum cooling and no land constraints. Starcloud's 60kg test satellite is already in orbit carrying an NVIDIA H100, and SpaceX filed with the FCC earlier this year for up to one million AI compute satellites. These ideas may sound impractical, but they're already attracting billions in capital.

Bottlenecks: high costs; obsolete ground infrastructure; unclear economic viability for larger-scale projects; SpaceX's near-monopoly in payload and commercial satellite infrastructure.

Our take: For humanity to reach its full potential, we must return to space. We landed on the moon in 1969 and never returned. Mars is the long-term dream, and beyond Mars, more speculative targets like Jupiter's moon Europa (with its subsurface ocean and the highest likelihood of microbial life in the solar system) and Saturn's moons Titan and Enceladus. But if we ever want to colonize our solar system, building a moonbase is the first real step. For such a space race to be at least partially economically viable, we will need a growing satellite industry, solar power relays, extraterrestrial resource mining, and eventually concepts like lunar mass drivers, electromagnetic catapults that could move material into orbit at near-zero marginal cost. While these may sound like sci-fi today, we dare to dream big.

We aim to keep investing in the most economically viable aerospace opportunities across the board, while being mindful of the challenging reality and long time horizons of space innovation. SpaceX is our core holding. We've also taken private positions in a company building ground-station infrastructure and a company providing microgravity biochemical manufacturing on orbit. We are looking at adjacent satellite infrastructure and orbital defence as potentially viable areas in the next 5 years, while remaining open to other ideas as they present themselves.

6. Biotech and Healthcare

Trend: Two structural facts shape this theme. First, demographics: populations in most developed countries are aging fast. There are more adults and elderly than children and teenagers. While this usually means less consumer spending, health and longevity are products humans aren't price sensitive to. Healthcare spending will rise on both the consumer and public sides. Many healthcare segments are well-developed and saturated; others, particularly chronic disease, rare disease, and personalised care, are chronically underserved. General practitioners are often overwhelmed by patients and don't have time to look into individual cases deeply enough, defaulting to treating symptoms and prescribing standardised treatments.

This is where AI becomes a game changer. LLMs make precision medicine economically viable for the masses. Customised diagnosis and treatment no longer require hours of a specialist's time per patient. On the research side, AI compresses the cycle of compiling existing knowledge, running meta-analyses, and identifying viable therapeutic targets, which has historically been the slowest and most expensive part of biotech R&D.

Bottlenecks: regulatory approvals and clinical trials; model quality (hallucinations); access to sensitive health data; market dynamics (big pharma domination).

Our take: Despite the clear benefits of biotech discoveries, investment successes in this segment have historically been rare and largely contained within mainstream pharma. We are betting on AI finally breaking this curse. As commoditised intelligence compresses the R&D cycle, long-tail biotech may finally realize its potential.

We are largely avoiding the overcrowded drug discovery space, focusing instead on precision medicine and AI-driven diagnosis, while paying attention to more sci-fi-like long-shots — nanotech, biological augmentation, and lifespan-prolonging treatments. To cover the early-stage longevity space specifically, we backed Age1 - a longevity focused VC.

7. Adversarial AI and negative externalities

Trend: AI brings revolution in productivity but also multiple vectors of disruption. The first is socioeconomic. AI is reshaping the knowledge-work labour market faster than any prior technological shift, with real potential to drive unemployment, social unrest, new political movements, and serious policy responses (universal basic income chief among them). The aggregate productivity story doesn't have to map to prosperity for every individual. AI may further exacerbate the K-shape economy, leading to a serious political fallout.

The second is digital. Agents and AI-generated content are saturating the internet and empowering bad actors, from criminals to adversarial nation states. Fake news, software exploits, scams, and fake identities are proliferating fast. The Dead Internet Theory — the idea that most online content is now bot-generated — stops being a meme and starts being a realistic assumption.

The third is civilisational. If AI propels scientific discovery far enough, it becomes capable of accelerating bioweapons design, novel pathogens, massive-scale cybersecurity exploits and other catastrophic-tail threats. We treat this as a low-probability, high-impact scenario and discuss it more in the bear case.

Our take: While the PC and internet eras brought us the antivirus paradigm, AI will introduce many more security and protection angles that will be essential to keep us safe. We expect the cybersecurity field to face disruption while also growing massively as an industry as the demand for new AI native security tools accelerates. National security frameworks will need to address adversarial AI threats; corporations will need to invest in the best cybersecurity products. Many online services will require users to prove their humanity through strong digital identity verification, as existing solutions can already be fooled by AI. We are looking to invest in opportunities across all of these vectors, with a particular focus on human identity solutions.

In the preamble we argued that AI unlocks won't favour new pure software startups. Cybersecurity is the cleanest exception. Defending against AI-driven threats requires solutions that genuinely don't exist yet, and the M&A path is open: big tech is going to keep acquiring the best startups in this space because they can't build fast enough internally. That gives early-stage cybersecurity startups one of the cleaner exit paths in tech right now. We've partnered with Tachles to identify the best opportunities here.

Bear cases, risks and caveats

Nothing is certain except death and taxes. So let's talk about the most likely ways we can get burned.

A. Geopolitical uncertainty overwhelms the tailwinds

The most likely version: a prolonged Hormuz blockade. Energy and commodity shortages globally, inflationary spike, broad economic drag. Moderately likely, painful but recoverable — most of our themes slow down rather than break.

The catastrophic version is the Taiwan Strait. If China moves against Taiwan, TSMC gets cut off and the global semiconductor supply chain breaks at its single most critical node. China simultaneously tightens its grip on commodities and materials, bans exports, and the military situation disrupts supply chains across APAC. Global trade grinds to a halt; both superpowers shift to wartime economies. This is bad for almost everything we've laid out, including defence on the production side, even as defence budgets surge. We treat this as a low-probability, high-severity scenario. We are looking to hedge this tail actively, and if probability rises, we adjust the public portfolio.

The third version is political rather than military: a US election shifts power to populists running on an explicit anti-AI / anti-growth platform, and the regulatory framework turns prohibitive. Less likely than the geopolitical scenarios in our view, but it would slow the tech industry substantially.

B. AI hype turns into an unproductive bubble

LLMs are incredible technology, but they're not immune to hype cycles. We are already seeing signs of froth: pre-revenue rounds at billion-dollar valuations, infrastructure deals priced for perfection, AI, space and robotics-themed SPVs and listings absorbing capital that wouldn't have moved this fast in a calmer cycle. Hardware manufacturers are repricing across the board. So far the Mag7 are funding most of this with real profits and real capex, which is what's keeping the cycle stable. The risk is straightforward: if productivity gains stall or if model quality plateaus, the funding flywheel breaks.

The silver lining here is twofold. Our experience navigating hype-driven crypto markets has conditioned us to look for signs of irrational exuberance and react accordingly. And even if AI progress plateaued today, there are enough productivity unlocks from present-day models to keep us optimistic within our 5-10 year time horizon.

C. The hardware cycle turns fast

This one isn't a thesis invalidation per se, but a critical timing question for the hardware-heavy part of our portfolio. We think the demand overhang runs into 2027, but we could be wrong on duration. Markets price these cycles forward, and the peak shows up in stock prices before it shows up in fab utilization or shipment data.

The factor that's been buying us time is what we'd call "cyclical PTSD": the foundries, memory makers, and equipment vendors who lived through the 2022 memory collapse and prior down-cycles are now reluctant to add capacity too fast. Their conservative approach is part of why the cycle may run longer than before. But if we see early signs of overproduction, we may already be looking at the top in the hardware names in the next few quarters.

We're watching for early signals: order book softening at the foundries, capex guidance changes from the major equipment suppliers, step function improvements in optimisation on the software side or other innovations reducing the hardware constraints. If we see more of those signals flashing, we'd rotate hardware exposure into the cycle-resistant parts of our book: software with structural moats, defence, biotech.

D. AI tail events

Bad actors may use AI to cause large-scale harm, pandemic-grade bioweapons, infrastructure attacks, large-scale fraud. Global authorities respond with a sweeping crackdown that slows AI innovation across the board. The probability is non-trivial and the impact is broad.

The other version is the p(doom) scenario: artificial superintelligence emerges with goals misaligned from humanity's, and we lose control of the most consequential technology we've ever built. On the opposite side of this tail lies singularity or an AI utopia, where money becomes obsolete and people don't work anymore. In which case whatever we do now doesn't matter either. It sounds funny, but there are smart people out there, including Elon Musk, who posit this scenario. We lack expertise to opine on the probability of such outcomes but it’s worth putting it out there.

Theme 7 in our portfolio is, in part, a hedge against the first scenario. Cybersecurity, agent governance, and identity verification all become more valuable in a world where adversarial AI is causing real harm. Obviously, we don't think anything can hedge us against the second.

E. Execution risk

We're not going to predict which scenarios play out. The portfolio is built and diversified for it: more than half of the NAV is in liquid public equities precisely so we can react when signals emerge, and the rest is allocated across themes that don't all break together.

The last risk worth raising is our own. Active managers may make mistakes, underperform, and miss the best opportunities. We've been wrong before and we'll be wrong again. What we'd argue is that being wrong while engaged is a better risk than being right by sitting out as the world changes under our feet.

In Conclusion

Sigil Supernova is deliberately diversified into: AI and adjacent hardware and software, deeptech and robotics, aerospace and defence, biotech and healthcare, and adversarial AI and cybersecurity. We will also not ignore idiosyncratic opportunities that escape neat labelling.

The portfolio combines public equities (more than half of NAV, across thematic baskets) with carefully selected private investments from seed to pre-IPO. The public side gives us liquidity and the ability to rotate as cycles progress; the private side gives us exposure to opportunities that haven't reached public markets yet. We're partnering with sector-focused VCs in areas where we don't have direct expertise so we can access the highest-quality early-stage flow without overextending our own bandwidth.

We expect every theme to go through its own hype cycle. Innovation sparks speculation, speculation overshoots, the bust arrives before the productive phase does. We've navigated such cycles before in crypto. We aim to use this experience to stay clear-headed.

The next 10 years will be transformational. We are ready for the ride. Are you?