Table of contents:

Sigil Core

In Q1 2026, Sigil Core returned:

- -3.88% net of fees against EUR

- -5.23% net of fees against USD

…and outperformed its BTC benchmark by 21.56% net of fees:

Dear Investors,

Since we are writing this letter with a slight delay and the benefit of hindsight, let us lead with words of reassurance: Sigil remains unaffected by the wave of hacks and exploits that hit the DeFi ecosystem in April. We will cover these events in depth in our next letter.

Turmoil Continues

Q1 2026 was another action-packed quarter. We saw conflict in the Middle East re-escalate. The USA and Israel attacked the Iranian regime, which was already weakened by previous strikes and domestic protests. However, the regime withstood the onslaught and was able to strike back, hitting its Middle Eastern neighbours allied with the West. The Iranian blockade of the Strait of Hormuz and attacks on key energy and natural resources infrastructure were particularly impactful. Global supply lines for oil, fertilizers and agricultural products, petrochemicals and plastics, and industrial materials such as sulfuric acid were all disrupted.

As a reaction, commodity prices spiked, led by oil and natural gas, but remained volatile in both directions as chaotic news about the conflict and ceasefire agreements kept changing the narrative. While the conflict has now entered a "cold phase," the uncertainty remains. We expect the economic reality of the disruption to have persistent effects on the markets. So far, markets seem to be shrugging the damage off, with semiconductors and AI infrastructure leading the risk-on bull market. While markets are unfazed, people in many countries are feeling the shortages first hand. If the Hormuz blockade continues, these shortages could turn into a real commodity and agricultural crises globally. There is still hope for a quick resolution and at muted negative outcomes, and we don't feel confident in our ability to analyse the situation better than macro and geopolitical experts, so let’s just say we are mindful of the risks and watch these events carefully.

Hyperliquid is a 24/7 exchange

During the conflict, Hyperliquid showcased its usefulness by providing 24/7 perpetuals for oil. It became the dominant price discovery venue for oil over the weekends, when regular exchanges were closed.

It’s not some “shady offshore trading” either. Hyperliquid-based Trade.xyz secured a license with S&P Dow Jones for official inclusion of their indices. Hyperliquid Policy Center was formed to act as an intermediary between Hyperliquid protocol and ecosystem on one side, and US regulators on the other side.

Are we timing the market?

Crypto volatility around the conflict in Iran was noticeable but not extreme. It seemed that crypto prices had already found a comfortable bottom, and we can expect a slow and selective recovery. This expectation leads us to start deploying our excess cash back into the market. At the start of 2026 we were 40% risk-off; now we are net buyers, slowly scaling into select assets.

From the above, it may sound like we aim to generate alpha by timing the market. This is usually not the case. When we consider the risk-on vs. risk-off ratio in our portfolio, we do so to manage risk, not to time the market per se. Last year we saw risk in crypto increase from multiple vectors: the October 10th liquidations revealed a structural weakness in crypto markets, forcing many market makers to play defensively, while new token unlocks kept increasing the overall supply. We also noticed "soft" signals from our network and conferences, revealing many crypto funds struggling to raise and having to liquidate. Crypto VC vintages of 2021 and 2022 were in a particularly bad spot, sitting on overvalued rounds from the peak of the mania. On a macro level, we foresaw conflicts accelerating, while global liquidity — a closely followed indicator in crypto circles — started showing weakness. The four-year cycle pattern, which often seems too simple to work, appears to be repeating for at least the 4th time in a row.

Compared to the end of last year, we currently perceive many of these risks as priced in, and the risk:reward of holding (some) crypto assets is improving. Thus, we are more comfortable with our standard exposure again. Long term, we don't believe market timing is a reliable source of outperformance under most circumstances. But as we grow and as the crypto market matures, we take a more nuanced view of risk management.

A note on volatility and risk

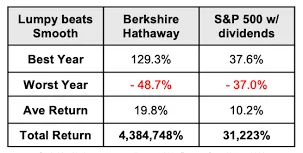

Sigil Core is an exceptionally volatile vehicle, with the value of its shares swinging wildly and historical drawdowns of up to 60%. This is partially caused by crypto assets being the most volatile liquid asset class in the world. Some of the tokens we hold and trade are akin to shares of early-stage startups, with a lot of execution risk. By nature, the risk profile of at least a portion of our book is close to that of a VC portfolio, with the main difference being (partial) liquidity and mark-to-market prices. If portfolio companies of traditional VCs were exposed to the same market-based pricing, they would look similar. While most tokens are still not equity per se, we are slowly getting there. And many tokens already reflect this disparity in price, offering attractive risk premia.

Another point is philosophical. Most capital allocators view volatility as a risk and are willing to overpay for protection against it, in effect giving up a big portion of the upside in order to "smooth the curve." This "institutional" preference often forces the portfolio manager to make compromises in their investment approach. That results in the portfolio manager's personal book, where there is no pressure to manage volatility, outperforming his fund.

But we don't have a personal book. All our crypto investments are in Sigil. We think volatility is an opportunity, not only for traders but also for long-term-minded investors. We agree with Warren Buffett: "preferring lumpy 15% over smooth 12%." Thus, we are reluctant to materially impair our upside in order to placate the low-volatility preference of some investors (this is also why we offer Sigil Stable: every investor can smooth the curve and/or attempt to time the market by splitting their exposure between Core and Stable).

We believe long-term investors should embrace the volatility and let the outperformance compound. Smooth curves are expensive and lead to mediocre absolute returns. (This goes for crypto and stock long bias investors, and is not directed towards credit, bonds, and market-neutral strategies)

The real risk we absolutely need to be mindful about (and to avoid) is the permanent loss of capital. This can happen mostly via idiosyncratic and systemic tail events hitting our biggest positions and the platforms we use. We are actively working to reduce these tail risks. Another risk we are always evaluating is recognising the market structure and crypto - specific risks. Simply put, sometimes crypto markets do not pay us enough premia for the risks we are taking while fully deployed.

Crypto is maturing…or is it?

In the last letter we said crypto is maturing and winners keep winning. That's one part of the story. The other part is that the top 100 crypto assets still include many nonsensically overpriced, sometimes even fraudulent or abandoned assets. Active and professional management of crypto exposure will still offer a lot of value to investors, especially to those who are not satisfied holding just BTC exposure but aim to be exposed to all the other exciting innovations blockchain technology offers.

Our overall expectation for crypto maturing was that it would start trading more like the stock market. While partially true, ironically, we are also seeing the stock market trading more and more like crypto: narrative- and retail-driven pumps, meme-stocks, Trump tweets leading to massive dumps or rallies, insiders front-running Iran news with size in oil.

Sigil Core is spread across crypto/blockchain stocks, mature and liquid crypto assets, and early-stage investments with asymmetric risk-reward. So even if the overall upside and volatility of Bitcoin may go down as it grows, we believe crypto will keep offering significant upside down the risk curve. It will just not be as easy to capitalize on as in previous cycles, when every token pumped during "altcoin season" regardless of quality. Pavel (our CEO) recently spoke about our active asset management at a conference in Gibraltar. You can check some highlights here.

Conclusion

We will continue allocating our excess cash into select opportunities across themes we identified as the most attractive. We expect a bumpy ride in crypto markets throughout summer, with AI hype and geopolitics continuing to capture headlines. We also expect a few crypto assets and themes to outperform massively, while the rest of the crypto market continues a slow bleed. Improved regulatory framework, institutional adoption and market consolidation will act as a secular tailwind. Same with stablecoins slowly becoming a step improvement in global fintech infrastructure. On the other hand, increased hacking risks thanks to AI advancements may pose a temporary headwind in some crypto segments such as DeFi, at least until cybersecurity tooling catches up.

We will expand more on the rise of AI-driven exploits and North Korean hackers, and what it means for crypto in our Q2 letter.

Sigil Stable

In Q1 2026, Sigil Stable returned 1% net yield against USD (2.44% against EUR), with a Sharpe ratio of 2.11.

Two defining themes dominated the market-neutral space in Q1. Let's start with the less exciting and definitely less optimistic one.

The Great Basis Squeeze

We did mention the basis trade in the Ethena section of our Q3 letter, but we never actually bothered to define it. So, for the uninitiated: a basis trade is a delta-neutral strategy where you buy a spot asset while simultaneously shorting its futures contract to harvest the price premium, effectively pocketing the funding rate paid by over-leveraged long speculators.

Market participants were blessed with abundant basis trade opportunities in Q4 '24, which picked up again last summer, albeit with slightly less intensity. But after the infamous October 10 liquidation event, the compression began and annualized funding rates entered a hangover state in Q1.

While BTC declined 22% last quarter and CEX spot volumes dropped almost 40% quarter-over-quarter, the BTC funding rate dropped by almost 50%, from roughly 4% to 2% and is down nearly 80% from its cycle peak.

Our allocation into this strategy bucket represented less than 8% of AUM at the end of Q1. We anticipate this will increase as we roll out new automated execution features, allowing us to capture smaller inefficiencies even if the broader market sentiment doesn't significantly shift.

The New Casino: TradFi and Commodities Perps

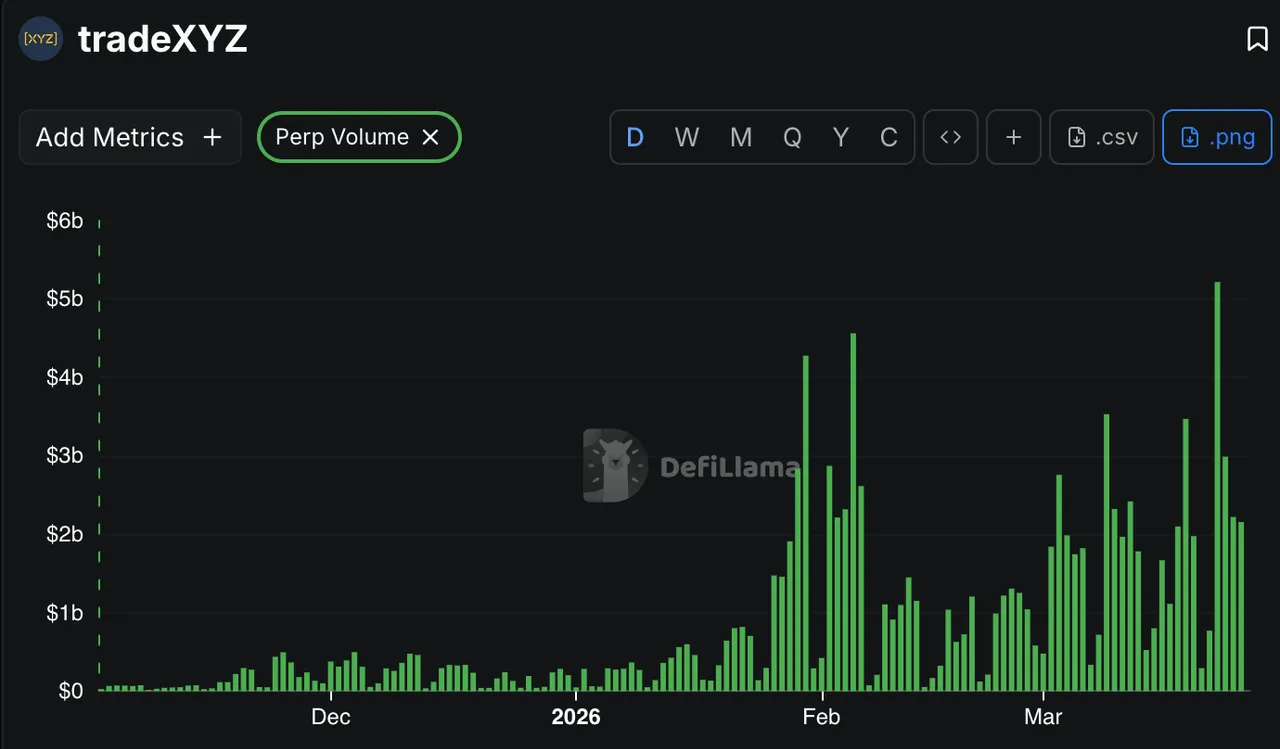

To follow up on Fiskantes's “Hyperliquid is a 24/7 exchange” section from earlier, the most exciting development last quarter was the explosion of activity on permissionlessly deployed markets (HIP-3) built on top of Hyperliquid, driven especially by the builders at trade.xyz.

Trade.xyz had its first massive breakout moment at the end of January, surpassing $4 billion in daily trading volume on the exact day the global gold market experienced the highest trading activity in its entire history.

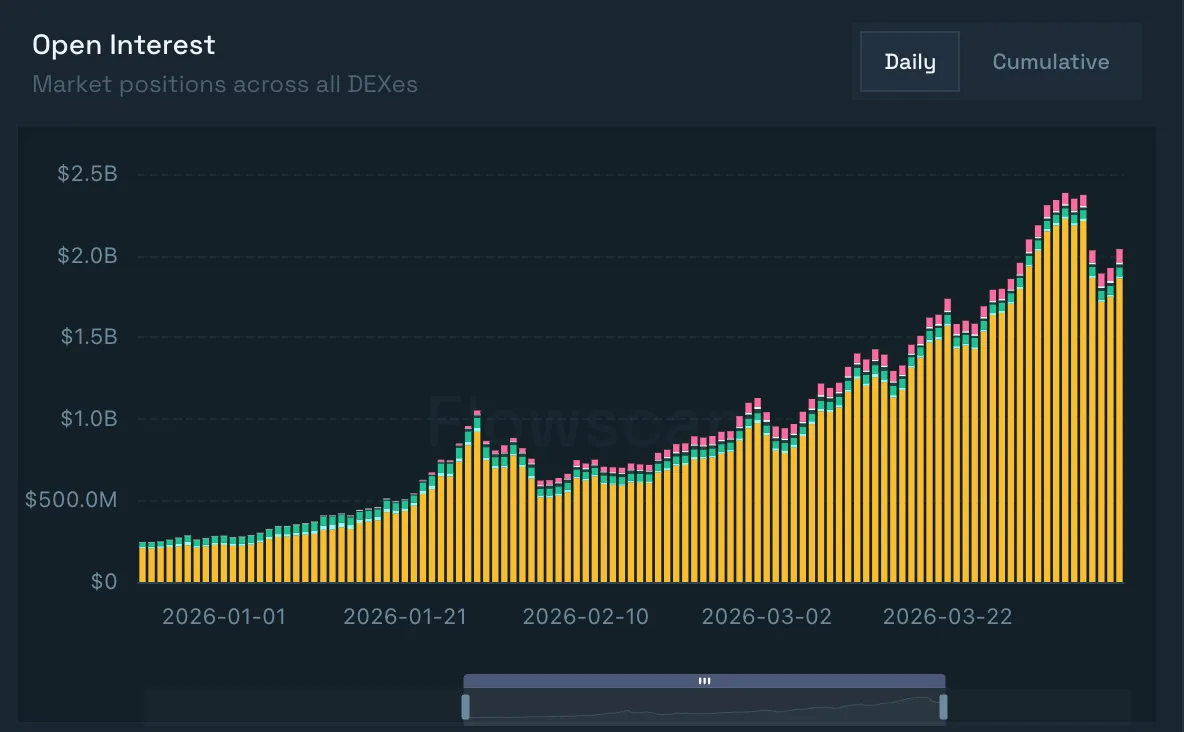

By March, tokenized equities and commodities represented the majority of the top markets in terms of open interest on Hyperliquid; crude oil, gold, silver, and S&P 500 contracts routinely sat in the top 10. Total open interest saw incredible growth, reaching almost $2.5 billion at its peak. Interestingly, crypto-native market makers became some of the largest liquidity providers to global commodity and equity index flows.

Beyond HIP-3, there are other venues facilitating real-world asset (RWA) trading that demand attention. Lighter is a prime example, Sigil Core holds its native $LIT token, and Sigil Stable is actively trading on the venue. While trade.xyz remains the undisputed heavyweight (for context, its crude oil market open interest is roughly 20x larger than Lighter's), the broader trend is undeniable.

From a market-neutral fund perspective, these venues are a source of structural inefficiencies: basis trades, cross-venue divergences, weekend dislocations, and index-oracle mismatches. On the other hand, these markets carry a different set of risks than crypto perpetuals. Oracles freeze. Liquidity vanishes. Funding rates can become highly volatile when the underlying reference market is closed, but the on-chain casino is still open.

We are actively deploying both manual and automated trading strategies across these on-chain RWA perp markets. While the capital allocated here hasn't been massive yet (except for the Ostium deal below), we anticipate that will change drastically in the coming quarters as the plumbing matures.

Ostium: The Broker, Not the Casino

Finally, we entered into a private liquidity deal with Ostium in Q1. Jump had already validated the broad thesis when they co-led Ostium's $20m Series A prior to our involvement. As usual, we cannot disclose the commercial terms, but the high-level thesis is worth sharing.

Ostium is one of the more interesting attempts to bring real-world asset trading on-chain. While many traders loosely bucket it together Hyperliquid or Lighter, Ostium is economically closer to a crypto-native CFD or broker business than a traditional exchange. It takes the other side of user flow, manages its own risk, and hedges exposure in the underlying TradFi markets.

That model comes with real complexity. Ostium’s biggest bottleneck today is not demand, but hedging capacity. Open interest caps are necessary because the protocol cannot responsibly scale user flow faster than its ability to hedge. This became obvious during the sharp move in precious metals earlier this year, when a five-sigma move stressed the hedging engine and exposed the limits of the previous architecture. Ostium has materially improved its capital efficiency, an upgrade made possible, in part, thanks to our partnership and injected liquidity.

The X post below is great proof that Ostium's upgraded engine can now accommodate significant institutional demand.

Conclusion

To wrap up Q1, Sigil Stable continues to pivot away from fleeting, synthetic yields and toward structural, infrastructure-level opportunities. This shift is clearly reflected in our portfolio composition: our allocation to private liquidity deals grew from 27% at the end of Q4 to 34% at the close of Q1. It is important to note that the vast majority of the rewards from these deals have not yet been realized in our PnL.

We are effectively planting seeds in the fastest growing segment on-chain: TradFi and commodities perp markets. As the broader market slowly wakes up from its basis-trade hangover, we are positioned exactly where the real, sustainable yield is being generated.

Thanks for your continued support.

PS: We’ve launched a new fund, Supernova, focused on backing humanity’s next major breakthroughs through frontier technology. We’ve published our thesis here. We’ve also launched a new website, we hope you like it!